Cleantech FY23 Recap And FY24 Outlook

None of this should be construed as investment advice and all opinions are my own personal macro observations. None of the below consists of independent stock opinions nor will I ever provide that. As 4Q23/FY23 earnings season comes to an end, I thought it'd be fitting to summarize some of the major trends going on with cleantech stocks as I've done in prior posts (Rates + Regulatory Overhang Weighing On Cleantech Stocks, Cleantech 3Q23 Recap & Outlook). Let's dive in. *Disclaimer - I use global clean indices as a barometer of performance but then only discuss US stocks as that's what I am closest to and have expertise in. Bottom-line upfront - Key Takeaways:

- It appears you're seeing a "flight to safety" with investors paying premiums for companies executing with strong operating performance vs. those facing more difficult growth outlooks (e.g., Nextracker vs. Array, Quanta vs. Mastec, Trane vs. Johnson Controls, etc.)

- Debate on the best way to get exposure to cleantech:

- Approach 1: Invest in incumbent businesses with climate-adjacent products/services (stable, less pure exposure to secular tailwinds)

- Approach 2: Invest in pure-play cleantech business (100% exposure to climate tech/decarbonization but a lot more volatility of stock and financial performance)

- Headline risk around elections and interest rates are surely to keep impacting equity performance

- Investors may start to take bets around "normalized earnings" or that "we have reached the bottom" on certain sectors like residential solar or lithium

- Note: "reaching the bottom" in public markets refers to anticipating the lowest point in a security's forward financial estimates, as determined by sellside analysts, to capitalize on an improved risk/reward opportunity for potential future gains

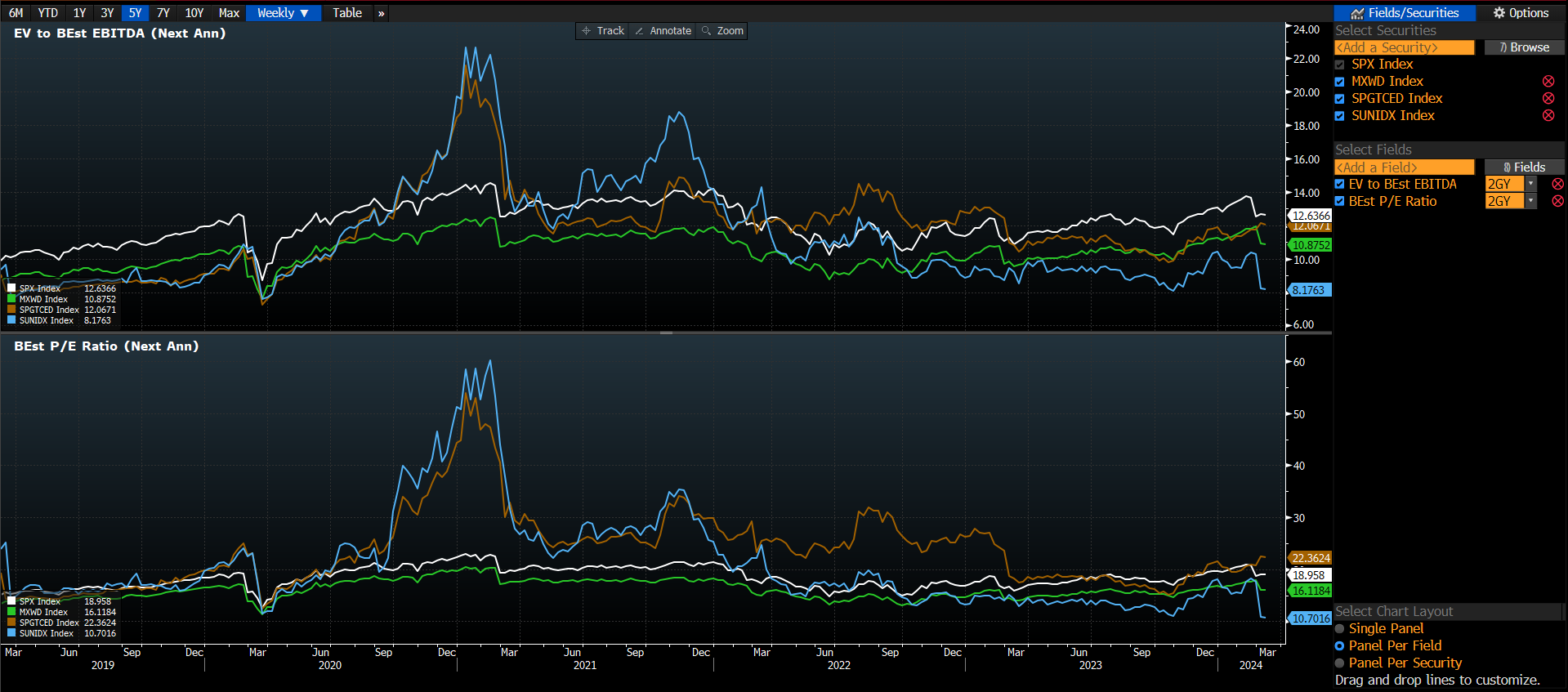

Performance: I use the S&P Global Clean Energy and the MAC Global Solar Index as barometers for global cleantech broadly. As you can see below, it's been a particularly challenging 2Y period with the cleantech indices underperforming the broader market by 40-50%+! Although broad market returns have been uniquely concentrated in a few stocks largely driven by the AI-hype, the point stands that cleantech has been incredibly challenged (especially, as recently the market has broadened out).

- SPX Index (White Line): The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities and serves as the foundation for a wide range of investment products.

- MXWD Index (Orange Line): The MSCI ACWI Index is a free-float weighted equity index. MXWD includes both emerging and developed world markets.

- SPGTCED (Yellow Line): The S&P Global Clean Energy Index is designed to measure the performance of companies in global clean energy-related businesses from both developed and emerging markets.

- SUNIDX (Red Line): MAC Global Solar Energy Index tracks globally-listed public companies that specialize in providing solar energy products and services.

Zooming out, over the prior 5-year period, you can see a lot of the run-up in some of these equities was in the 2020-2021 period which was driven by multiples expanding rapidly. This was a combination of low interest rates, market hype around the secular story for clean energy, and rapid growth rates in markets like residential solar, global EV adoption, etc.  When unpacking performance over the time period, you can see how the indices fared against other S&P industry sectors in terms of how much of their growth came from EBITDA growth vs. EV/EBITDA multiple expansion (e.g., look at the brown and blue lines for the S&P Global Clean Energy and MAC Global Solar Energy Indices, respectively, versus the S&P 500 and the MSCI ACWI lines [white and green lines, respectively]).

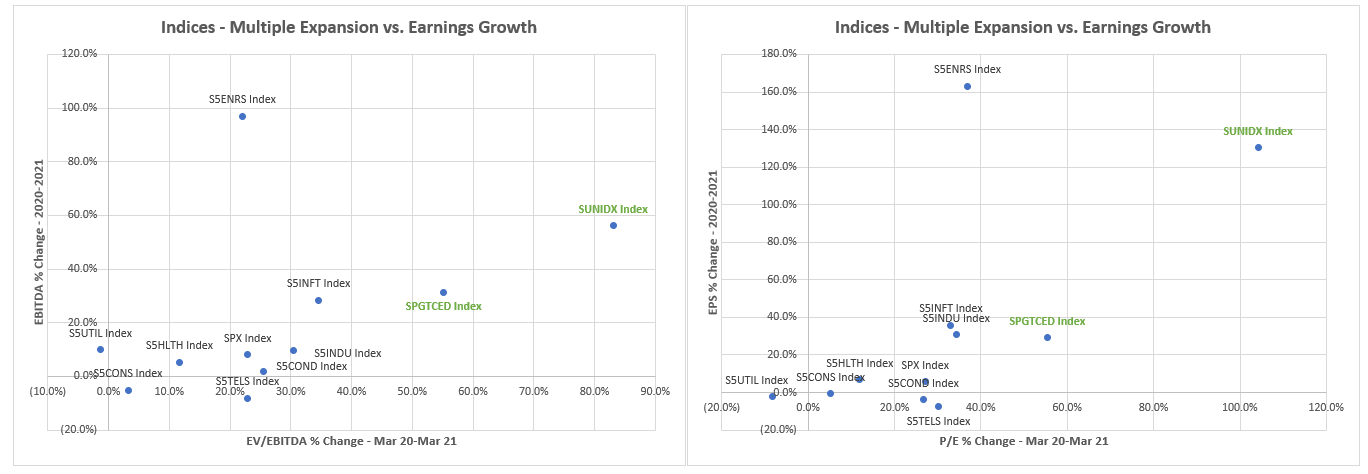

When unpacking performance over the time period, you can see how the indices fared against other S&P industry sectors in terms of how much of their growth came from EBITDA growth vs. EV/EBITDA multiple expansion (e.g., look at the brown and blue lines for the S&P Global Clean Energy and MAC Global Solar Energy Indices, respectively, versus the S&P 500 and the MSCI ACWI lines [white and green lines, respectively]).  As you see above & below, a lot of the March 2020- March 2021 valuation expansion was driven mostly off of multiple expansion vs. earnings growth for the cleantech indices versus other major sectors (highlighted in green; SPGTCED = S&P Global Clean Energy Index, SUNIDX = MAC Global Solar Index)*.

As you see above & below, a lot of the March 2020- March 2021 valuation expansion was driven mostly off of multiple expansion vs. earnings growth for the cleantech indices versus other major sectors (highlighted in green; SPGTCED = S&P Global Clean Energy Index, SUNIDX = MAC Global Solar Index)*.  *Note: The S&P500 can be split up be GICS (Global Industry Classification Standard) sectors, which are charted below and include: Energy (S5ENRS), Industrials (S5INDU), Information Technology (S5INFT), Consumer Discretionary (S5COND), Utilities (S5UTIL), Consumer Staples (CONS), Healthcare (S5HLTH), Communication Services (S5TELS). What's driving the underperformance recently? I've broken this down in prior posts but the main factors are:

*Note: The S&P500 can be split up be GICS (Global Industry Classification Standard) sectors, which are charted below and include: Energy (S5ENRS), Industrials (S5INDU), Information Technology (S5INFT), Consumer Discretionary (S5COND), Utilities (S5UTIL), Consumer Staples (CONS), Healthcare (S5HLTH), Communication Services (S5TELS). What's driving the underperformance recently? I've broken this down in prior posts but the main factors are:

- Higher interest rate environment: Interest rates impact cleantech in a multitude of ways including at a customer point of purchase (e.g., higher overall cost for debt-financed residential solar system or EV) or at the corporate level (e.g. higher interest expense and cost of capital for businesses with a high degree of capital intensity)

- Geopolitical/geo-economic considerations:

- Russian invasion of Ukraine spiked up global energy prices which influences the attractiveness and adoption rate for things like solar and EVs

- COVID dramatically impacted supply chains which caused disruptions that lengthened lead times and accelerated orders. As supply chains normalized and inventories can lower to more typical levels, there is ongoing "destocking" effects across many industrial markets.

- Changing regulatory environment/subsidy schemes: Whether in the US with California (~40% of US residential market) moving from NEM 2.0 to NEM 3.0 (reduced incentives and longer payback for solar-only systems) or Europe with various removing/letting subsidies lapse (e.g., Germany solar subsidies, Italian superbonus tax credit expiry, etc.), or election uncertainty (~40% of the global population votes this year with implications around global clean energy policies)

- In the US, investors are grappling with what a Democratic or Republican win can mean for the durability of the IRA tax credits or what the chances of a full repeal look like, future policy around the import of Chinese-made products (e.g., solar panels, EVs) and potential tariffs

- While hard to draw out how much pressure to the sectors might stem from the polarization/politicization of ESG, it is important to note that they present material headwinds to fund flows and thereby can indirectly influence performance

- Idiosyncratic factors: Things like channel inventory destocking (residential solar equipment), supply additions outpacing demand (e.g., lithium markets), project delays (e.g., utility-scale solar) impact specific markets as we'll get into below.

You can see the performance of the same indices with the US 10YR and Henry Hub spot price overlaid. Notice how as interest rates stabilized at higher levels and as Henry Hub (US benchmark for natural gas) normalized lower, equities have continued to see pressure.

- SPX Index (White Line): The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities and serves as the foundation for a wide range of investment products.

- MXWD Index (Dark Blue Line): The MSCI ACWI Index is a free-float weighted equity index. MXWD includes both emerging and developed world markets.

- SPGTCED (Red Line): The S&P Global Clean Energy Index is designed to measure the performance of companies in global clean energy-related businesses from both developed and emerging markets.

- SUNIDX (Purple Line): MAC Global Solar Energy Index tracks globally-listed public companies that specialize in providing solar energy products and services.

- USGG10YR Index (Yellow Line): Treasury bond yields (or rates) are tracked by investors for many reasons. The yields are paid by the U.S. government as interest for borrowing money via selling the bond. The 10-year Treasury yield is closely watched as an indicator of broader investor confidence.

- NGJ24 COMB Comdty (Light Blue Line): The Henry Hub pipeline is the pricing point for natural gas futures on the New York Mercantile Exchange. The settlement prices at Henry Hub are used as benchmarks for the entire North American natural gas market and parts of the global liquid natural gas (LNG) market.

Sector Takeaways & FY24 Outlooks: "Climate-adjacent" multi-industrial companies remains positive:

- Companies see strong demand due to decarbonization, electrification, energy efficiency spending, reshoring trends (e.g., HVAC, Electrical, Automation; Trane Technologies, Eaton, etc.)

- Orders remain strong despite some concerns about the sustainability of backlog levels at multi-year highs

Solar is a mixed bag with some seeing selective opportunities while others face headwinds: Utility-scale Q is "who can avoid delays and execute?" while Residential Q is "are we at the bottom?"

- Utility-scale solar expected to be more resilient due to long-term demand drivers but are facing delays caused by financing, permitting, jammed interconnection queues, and transformer lead times. Divergent path between companies that are executing pointing to ~20% growth (Nextracker, Quanta) whereas other companies guiding more towards HSD type growth (e.g., Array, Shoals, MYR Group)

- Market forecasts in HSD-mid-teens range after a +60% year in 2023 (e.g., partially due to timing as 2022 was down due to regulatory delays)

- Residential solar companies struggle with channel issues and financing challenges. Focus is on near-term cash generation, cutting costs, and flushing out excess inventory in the channel. Some management teams calling the bottom mid-year (e.g., Enphase) whereas others say year-end (e.g. SolarEdge)

- Market going from multiple years of 20-30%+ growth from 2019-2023 to potentially down as much as mid-teens (-15%) in '24.

Electric Vehicles face a "gloomier" outlook than what was forecasted 12-18 months ago

- After growing ~100% in 2021, ~60% in 2022, and ~30% in 2023, global EVs (BEV+PHEV) expected to grow at ~20% in FY24

- Dramatic calls for 50% global penetration (EVs as a % of new vehicle sales) by 2027-2028 being pushed back out to 2030 or beyond

- Current penetration stands at low 30%s China, mid-20%s across Europe, and high single digits% in the US

- OEMs have been reducing/removing volume guidance or targets around EVs, slowing/pausing investments into EV production, and/or keeping production flat (e.g., Tesla - "in between two demand waves" comment or Rivian holding production flat)

Lithium price at 'unsustainable' levels but timing of return to demand re-acceleration and market deficit is uncertain.

- Prices rose in March due to increased demand and supply disruptions (e.g., environmental checks in Yichun region in China) but remain ~80% below the record high levels of 2022 at ~$15kg (vs. $80kg at record highs)

- Prices at current levels are unsustainable and are even causing Tier 1 producers (e.g., Albemarle, Arcadium, etc.) to guide to negative FCF years and will not incentivize future supply additions beyond projects already underway

- Long-term price trends are unclear as supply (30-40% last year and this year) is outpacing demand growth (35% last year vs. 20% this year) and many producers find themselves in advanced stage capex development cycles where it would cost more to stop than it would to keep spending

Potential for IRA repeal/curtailment poses significant risks:

- Different clean energy segments face varying levels of risk. Policy changes could significantly impact investment and growth in the sector.

- Based on various broker reports and events, a reasonable summary of view is below:

- High risk of impact: EV sales credits (30D, 45W), clean hydrogen production (45V), sustainable aviation fuel (40B), clean fuel (45Z), methane fees, adders for disadvantaged communities and union jobs, as well as spending on federal grants/spending [e.g., GHG Reduction Fund]

- Moderate risk of impact: Residential clean energy, including heat pump and efficiency credits (25D, 25C)

- Low risk of impact : Clean energy manufacturing credits (45X), solar and wind production (45Y, 48D), Nuclear (45U), Carbon Capture and storage and direct air carbon capture (45Q)

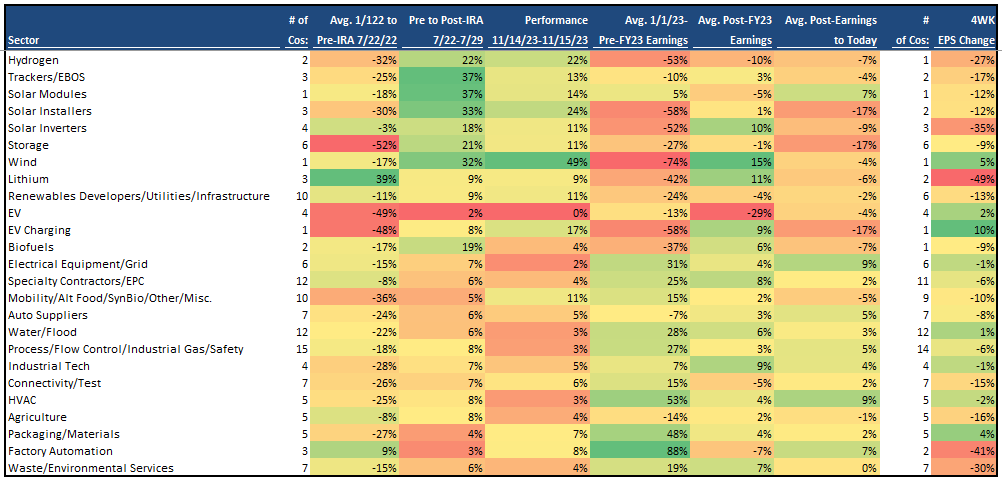

Share Price Reactions by Theme: Going back a few years, I thought it'd be interesting to look at the various clean energy stocks in the US by theme (e.g., bit subjective as to how/what you define as climate and clean energy) to see what they did before the IRA announcement, after it as passed, when there were increased expectations around rate cuts (e.g., Nov-23), 2023-2024 pre-FY23 earnings reports, post-earnings, and post-earnings to today. Below you can see a table that shows that exact information, with some key observations:

- Cleantech stocks were doing poorly in 2022 (as a result of the aforementioned factors) before the IRA was announced

- The week the IRA was announced, you saw a 20-30% jump in some specific themes impacted by the IRA

- Over the course of 2023 into early 2024, underperformance continued with some themes being down more than -50%

- The one jump was when there was market excitement around the possibility of multiple rate cuts in 2024 where certain themes jumped 10%+

- Post-earnings (day before measured to day after), themes have diverged in terms of some moderately up (e.g., storage, lithium) while others are down/mixed (e.g., solar)

- Many sectors remain weak post-earnings and even the ones with gains have since given them back

- Throughout the period, the "climate-adjacent" multi-industrial markets have held up a lot better

- Sectors like Electrical, EPC, Water, HVAC, Packaging, Automation, etc.

Final Thoughts The cleantech sector has faced significant headwinds over the past couple of years due to a confluence of factors like higher interest rates, supply chain issues, regulatory changes, and slowing demand in subsegments like residential solar and EVs. As the market looks ahead, there is debate on the best way to gain exposure to cleantech, with options including investing in incumbent businesses with climate-adjacent products/services or pure-play cleantech businesses. While the Inflation Reduction Act provided an initial boost, the sector has continued to underperform as execution challenges, policy uncertainty, and concerns around future demand weigh on companies. However, "climate-adjacent" businesses with exposure to areas like energy efficiency, electrification, and automation have shown more resilience. As the sector navigates this turbulent period, investors appear to be favoring companies with strong operations and reliable execution over pure-play cleantech firms grappling with more volatility. Despite the uncertainties, the long-term outlook for the sector remains positive as global efforts to combat climate change should continue to drive demand for clean technologies but investors will grapple with near-term challenges and potential policy changes.

Final Thoughts The cleantech sector has faced significant headwinds over the past couple of years due to a confluence of factors like higher interest rates, supply chain issues, regulatory changes, and slowing demand in subsegments like residential solar and EVs. As the market looks ahead, there is debate on the best way to gain exposure to cleantech, with options including investing in incumbent businesses with climate-adjacent products/services or pure-play cleantech businesses. While the Inflation Reduction Act provided an initial boost, the sector has continued to underperform as execution challenges, policy uncertainty, and concerns around future demand weigh on companies. However, "climate-adjacent" businesses with exposure to areas like energy efficiency, electrification, and automation have shown more resilience. As the sector navigates this turbulent period, investors appear to be favoring companies with strong operations and reliable execution over pure-play cleantech firms grappling with more volatility. Despite the uncertainties, the long-term outlook for the sector remains positive as global efforts to combat climate change should continue to drive demand for clean technologies but investors will grapple with near-term challenges and potential policy changes.