Exxon-Denbury and Broader Energy Transition Takeaways

In light of the Exxon acquisition of Denbury for $4.9BN ($89.45/share) this AM, I just wanted to share some broader reflections as it pertains to O&G companies and the energy transition and how different approaches and transactions can be evaluated. Exxon bought DEN at effectively no premium to prior close (although +19% from late Sept pre-deal rumors―many investors definitely underwrote some type of M&A event here) and had assets positioned to benefit from the rapid scale-up of the CCUS (carbon capture, utilization, and storage) industry. This insinuates that O&G companies can deploy capital opportunistically when the market is unwilling to pay up for a growth or sustainability story within a sector. This can creative attractive opportunities to invest in assets with long runways-that can also help them with sustainability goals- by investing capital into categories that can mature into viable businesses if these sectors take off. I broke it up into relevant sections broken out below if only one area appeals to folks:

- Exxon Low-Carbon Strategy

- Molecules vs. Electrons

- Carbon Capture’s Role in Energy Transition

- 45Q – A Gamechanger

- CCUS Hubs & Exxon Ambitions

- Denbury’s Pipeline a Strategic Asset in Scaling CCUS

- Significance to Future Business

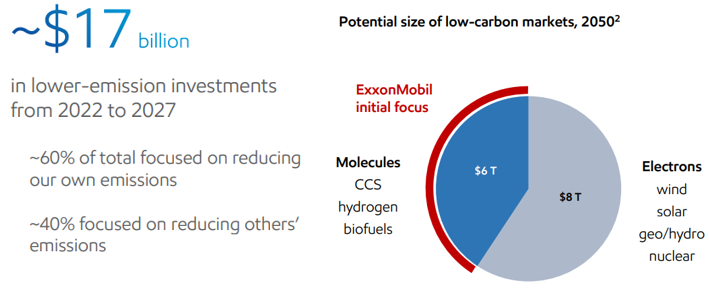

Exxon Low-Carbon Strategy In April, Exxon laid out a goal to spend ~$17 billion in lower-emissions investments over the next 5 years and they’ve targeted molecules ($6 trillion market according to Exxon) over electrons ($8T estimate). The latter point is quite important in my view since there’s a growing divergence between American and European operators and how they are approaching their transition which I’ll get into below. But the Denbury deal is one of several moves they’ve made in CCS, indicating their desire to be a leader in scaling up and providing the infrastructure for that industry. Given the deal and recent investments, Exxon is taking a buy AND build approach.

- ExxonMobil signs carbon capture agreement with Nucor Corporation, reaching 5 MTA milestone

- It’s the third carbon capture agreement we’ve announced in the past seven months, following previous ones with industrial gas company Linde and CF Industries, maker of agricultural fertilizer.

- It also marks a milestone – bringing the total CO2 we’ve agreed to transport and store for third-party customers to 5 million metric tons per year (MTA).

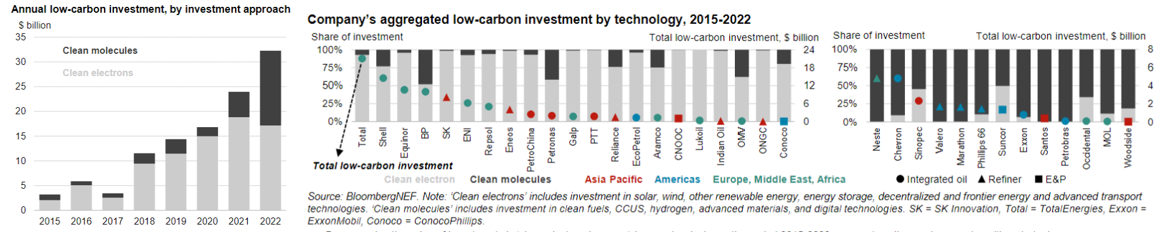

Molecules vs. Electrons To date, a broader classification for O&G approaches to the energy transition include the ‘clean molecule’ vs. ‘clean electron’ approach. BNEF has some useful data & takeaways, summarized below.

Molecules vs. Electrons To date, a broader classification for O&G approaches to the energy transition include the ‘clean molecule’ vs. ‘clean electron’ approach. BNEF has some useful data & takeaways, summarized below.

- Clean electron approach, which includes investments in renewable energy and electrification.

- This approach has been underlined by aggressive investments in renewable energy technologies, particularly solar and wind, over the past eight years. It also suggests a major strategic shift for companies, which seem unlikely to maintain oil and gas production as their main business in the future

- The largest investors in energy transition within the sector are typically the global/European-based integrated operators – led by and TotalEnergies, Shell, Equinor, SK Innovation, Eni and Repsol.

- Clean molecule approach, which includes investments in technologies that either reduce carbon emissions from fossil-fuel production, like carbon capture, utilization, and storage (CCUS), or produce lower-carbon alternatives that displace the fossil fuel currently in use, like biofuels.

- US majors Chevron and ExxonMobil are at the forefront of ‘clean molecules’ investment. They are joined by refiners in Europe and the US, notably Neste, Valero, Marathon Petroleum and Phillips 66. The US majors, despite boasting smaller low-carbon investments than their European peers, have charted a divergent path in energy transition by prioritizing low-carbon technologies that synergize with their oil and gas production, such as CCUS, hydrogen and renewable fuels. This may indicate that the majors are likely to continue prioritizing oil and gas production in their long-term strategy.

- This is now growing faster as these technologies now have some regulatory support and have greater synergies with O&G companies’ existing assets.

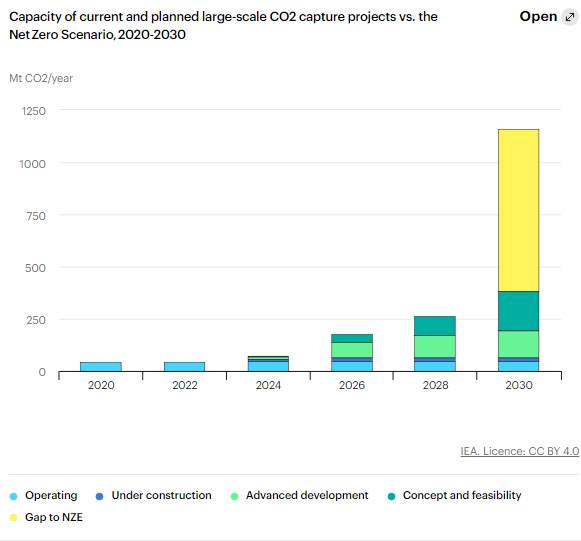

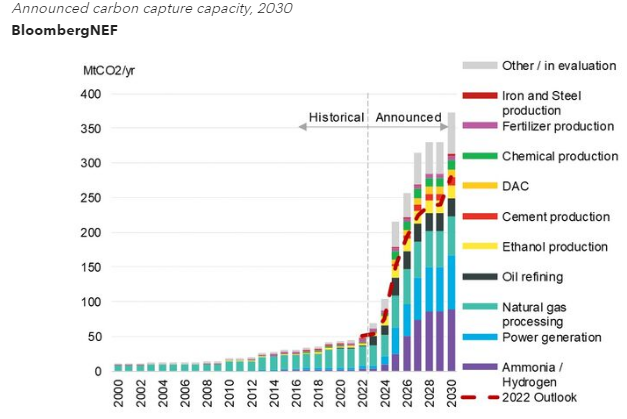

Carbon Capture’s Role in Energy Transition IEA’s latest report on CCUS is helpful in defining CCUS and its Role:

Carbon Capture’s Role in Energy Transition IEA’s latest report on CCUS is helpful in defining CCUS and its Role:

- What is it? CCUS involves the capture of CO2, generally from large point sources like power generation or industrial facilities that use either fossil fuels or biomass as fuel. If not being used on-site, the captured CO2 is compressed and transported by pipeline, ship, rail or truck to be used in a range of applications, or injected into deep geological formations such as depleted oil and gas reservoirs or saline aquifers.

- What is the role? CCUS can be retrofitted to existing power and industrial plants, allowing for their continued operation. It can tackle emissions in hard-to-abate sectors, particularly heavy industries like cement, steel or chemicals. CCUS is an enabler of least-cost low-carbon hydrogen production, which can support the decarbonization of other parts of the energy system, such as industry, trucks and ships.

- Why haven’t we done this before? Simple – it costs a lot and there previously wasn’t much economic incentive to cover/reduce costs. Capex to install equipment, Opex to run equipment and separate/process/transport/store CO2, etc.

- What changed? Among others, increasing regulatory incentives (45Q in the US) and global pressure to decarbonize heavy emitting sectors is driving the rapid scaling of the industry.

- History? The most high-profile CCUS projects in the past have been on coal generation plants. Early technical difficulties and an association with coal gave CCUS a poor reputation. However, there are several industries where CCUS is almost unavoidable if operators wish to decarbonize their processes (e.g., petrochemicals, ammonia, cement, etc.).

- Where are we headed? There are now around 40 commercial capture facilities in operation globally, with a total annual capture capacity of more than 45 Mt CO2 and that is expected to ~6x to ~300+ MtCO2/year by 2030

- NOTE: This is different than DACS.

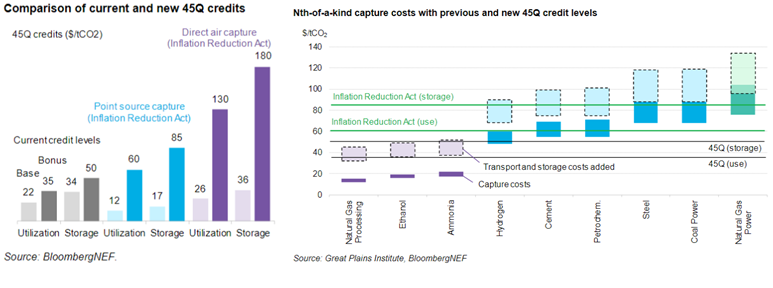

45Q – A Gamechanger In the Inflation Reduction Act, there was a revision of the 45Q tax credit for CCUS. It was a broadly bipartisan mechanism since it reduced emissions and is mostly used by the energy, power, and ag sectors. Some useful points from BNEF below from when the IRA was signed into law.

45Q – A Gamechanger In the Inflation Reduction Act, there was a revision of the 45Q tax credit for CCUS. It was a broadly bipartisan mechanism since it reduced emissions and is mostly used by the energy, power, and ag sectors. Some useful points from BNEF below from when the IRA was signed into law.

- The new legislation raised the credits for captured CO2 that is used and stored to $60/tCO2 and $85/tCO2 respectively.

- These credits will be split between the operators that capture, transport, and store the CO2 – of which Exxon plans to take a large share of.

- The new uplift to 45Q credits makes CCUS viable for a much larger number of industries, a key benefit of the new policy. While 45Q could previously only cover capture, transport and storage costs for high-concentration CO2 sources like natural gas processing, ethanol and ammonia, the higher credits for storage would allow blue hydrogen, cement, petrochemical and steel plants to offset much of their CCS costs, lowering one barrier to decarbonization.

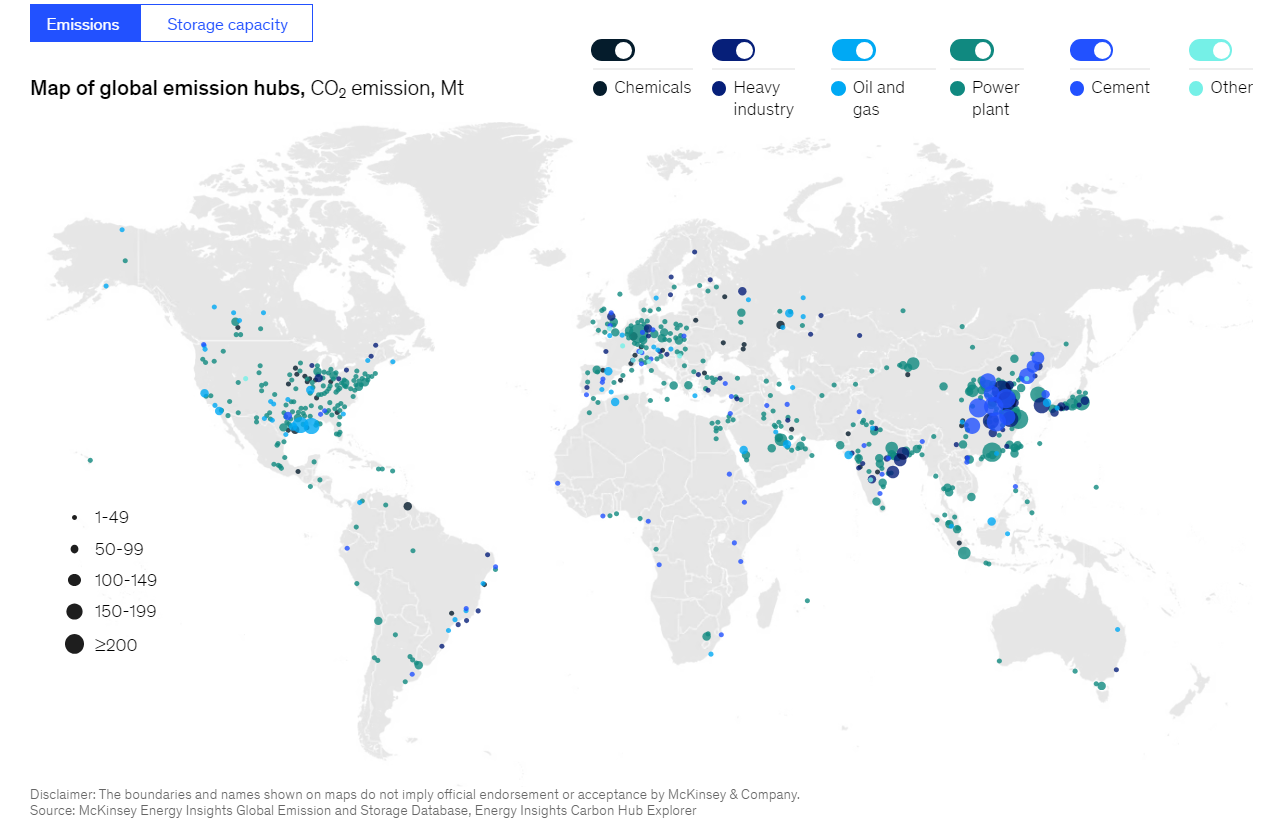

CCUS Hubs & Exxon Ambitions As CCUS economics are dependent on concentration of co2 stream, proximity to storage/utilization, transportation distance/options, location and infrastructure are very important to making economics more attractive. An important part of CCUS growth is the emergence of clusters of emitters hoping to use CCS to decarbonize known as CCS ‘hubs’. Hubs are particularly common for industrial emitters, as physical goods producers already naturally cluster around ports in order to receive feedstock and distribute their product. These arrangements have a number of benefits: sharing transport & storage costs, co-locating supply and demand with CO2 producers and consumers in the same area, increasing access to government funds, and benefiting from developers oversizing storage locations. The US is attractive from a source of stationary CO2 emission standpoint as well as being blessed with some of the largest/best-suited CO2 storage in the world. The Midwest and Gulf Coast are clear options for hubs based in the US and appear to be where Exxon is focused on evidenced by the Denbury deal and their other announcements in the area.

CCUS Hubs & Exxon Ambitions As CCUS economics are dependent on concentration of co2 stream, proximity to storage/utilization, transportation distance/options, location and infrastructure are very important to making economics more attractive. An important part of CCUS growth is the emergence of clusters of emitters hoping to use CCS to decarbonize known as CCS ‘hubs’. Hubs are particularly common for industrial emitters, as physical goods producers already naturally cluster around ports in order to receive feedstock and distribute their product. These arrangements have a number of benefits: sharing transport & storage costs, co-locating supply and demand with CO2 producers and consumers in the same area, increasing access to government funds, and benefiting from developers oversizing storage locations. The US is attractive from a source of stationary CO2 emission standpoint as well as being blessed with some of the largest/best-suited CO2 storage in the world. The Midwest and Gulf Coast are clear options for hubs based in the US and appear to be where Exxon is focused on evidenced by the Denbury deal and their other announcements in the area.

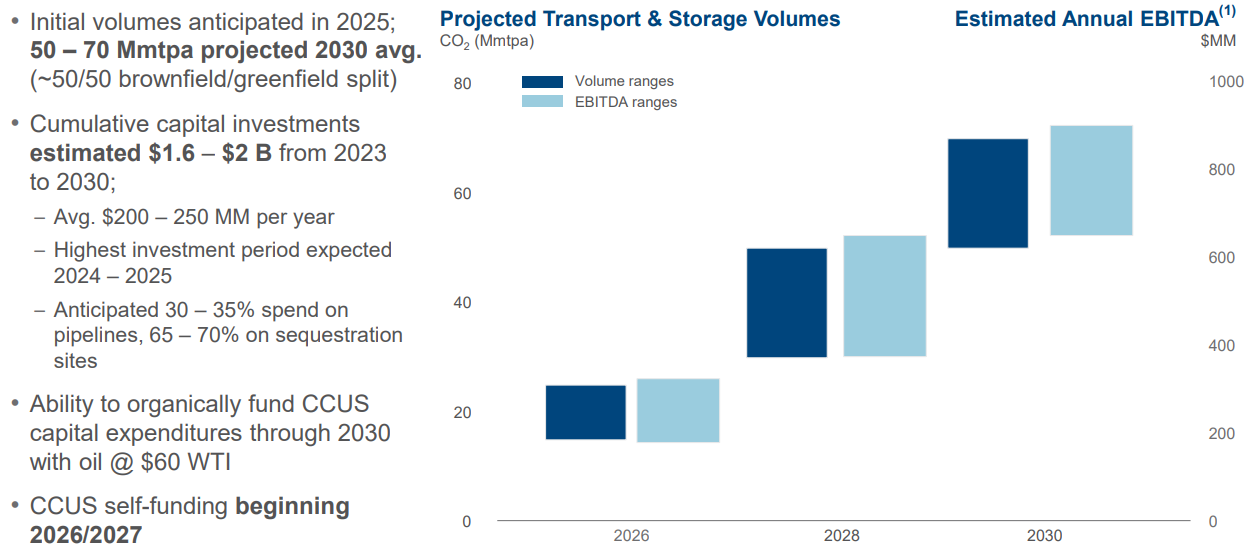

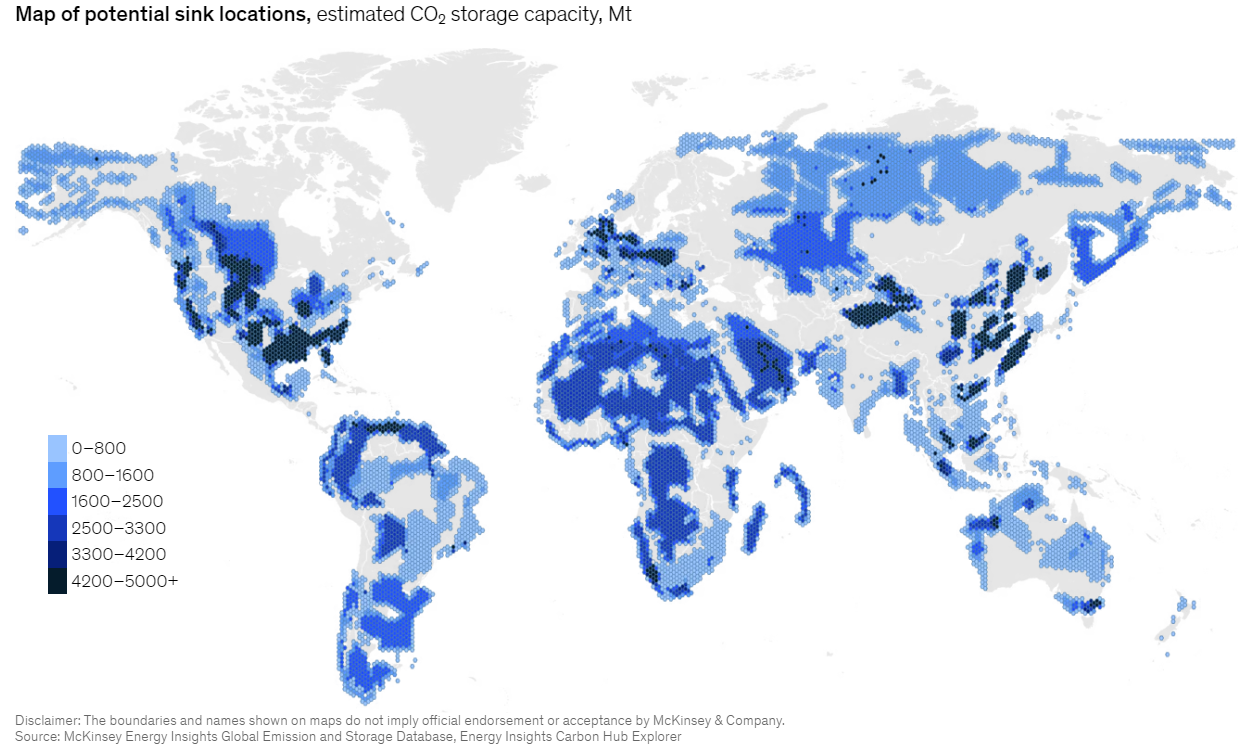

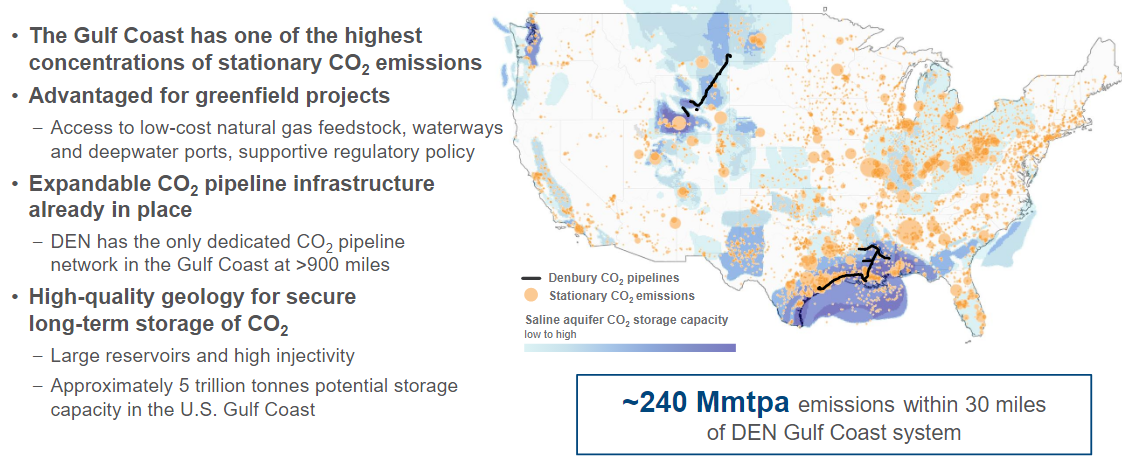

Denbury’s Pipeline a Strategic Asset in Scaling CCUS Enter Denbury and their CO2 pipelines. Denbury has >1,300 miles of existing DEN CO2 pipelines (~25% of existing U.S. total) specifically built for purpose of moving CO2 (you can’t just pipe CO2 in natural gas pipeline for example) and they separately have 7 sequestration sites with ~2 billion metrics tons of storage potential. The network has a transport capacity (incl. future planned expansions) of ~150 Mmtpa (million metric tons per annum) with existing capacity and extensions along the Texas Gulf Coast up to New Orleans and southwest Alabama and claims there is ~240 Mmtpa of emissions within 30 miles of their Gulf Coast System already. Their other pipelines connect the Rockies and Northern Plains regions. Replicating these systems would be challenging to do economically (management estimates $2-$4 billion alone) before considering all the regulatory burdens of trying to build new pipelines in the US.

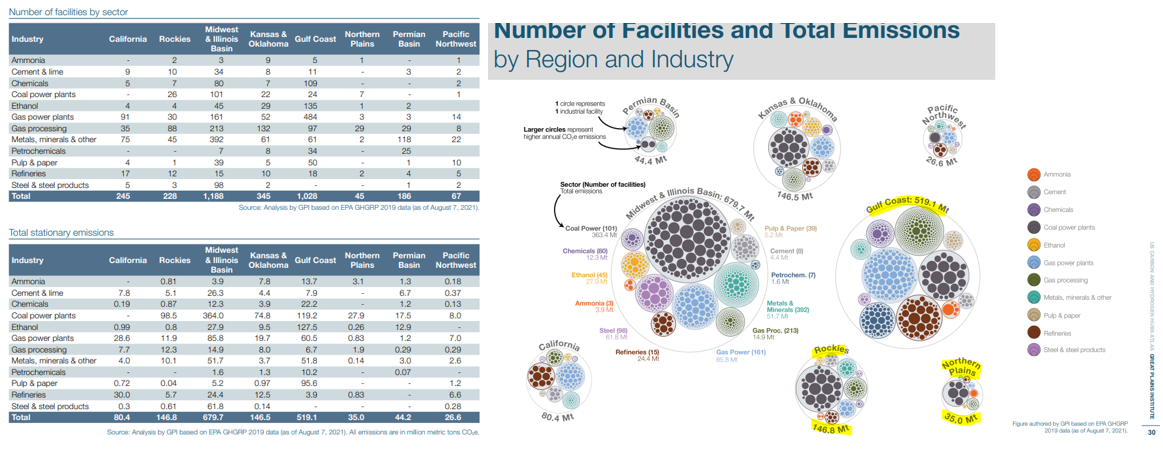

Denbury’s Pipeline a Strategic Asset in Scaling CCUS Enter Denbury and their CO2 pipelines. Denbury has >1,300 miles of existing DEN CO2 pipelines (~25% of existing U.S. total) specifically built for purpose of moving CO2 (you can’t just pipe CO2 in natural gas pipeline for example) and they separately have 7 sequestration sites with ~2 billion metrics tons of storage potential. The network has a transport capacity (incl. future planned expansions) of ~150 Mmtpa (million metric tons per annum) with existing capacity and extensions along the Texas Gulf Coast up to New Orleans and southwest Alabama and claims there is ~240 Mmtpa of emissions within 30 miles of their Gulf Coast System already. Their other pipelines connect the Rockies and Northern Plains regions. Replicating these systems would be challenging to do economically (management estimates $2-$4 billion alone) before considering all the regulatory burdens of trying to build new pipelines in the US.  When you compare that to the number of facilities and emissions in those regions, there are a considerable amount of facilities and emissions to address there. GPI Atlas of Carbon Hubs. According to the table below, there would be 1,028 facilities and 519.1 MT of emissions in just the Gulf Coast region alone!

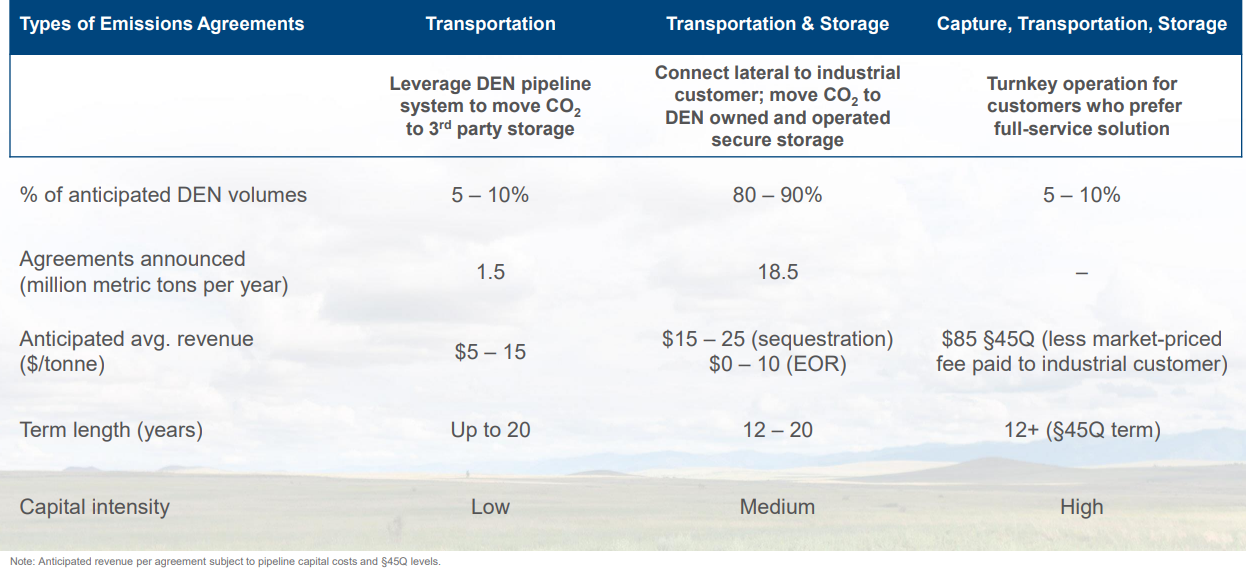

When you compare that to the number of facilities and emissions in those regions, there are a considerable amount of facilities and emissions to address there. GPI Atlas of Carbon Hubs. According to the table below, there would be 1,028 facilities and 519.1 MT of emissions in just the Gulf Coast region alone!  Significance to Future Business To be clear – the CO2 & transport business was only generating ~$60M of revenue for Denbury to date, which was not material to Denbury’s business today let alone a business of Exxon’s size. However, as CCUS markets take off and there is increasingly pressure for O&G companies to invest capital into the transition, Exxon is betting that the clean molecules market will scale up over time and can be an attractive business for them to build scale in. To figure out how much revenue the business can generate, it ultimately depends how much revenue per ton they can get and which services they provide. In their 2022 CCUS Business Outlook Deck, Denbury laid out 90% of volumes providing transportation and storage getting $15-$25/ton (+$10/ton when used for EOR) and 10% transportation only getting $5-$15/ton.

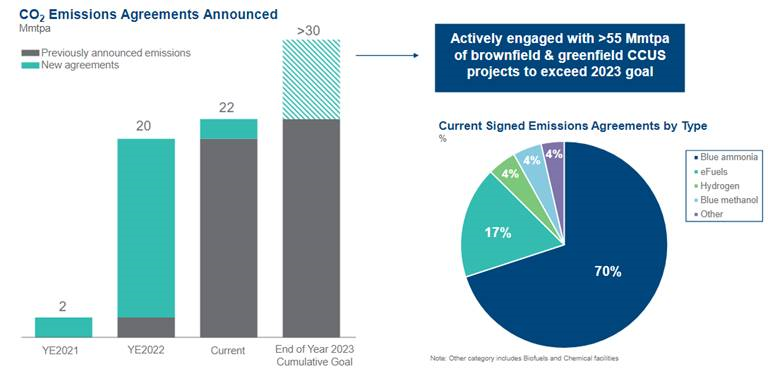

Significance to Future Business To be clear – the CO2 & transport business was only generating ~$60M of revenue for Denbury to date, which was not material to Denbury’s business today let alone a business of Exxon’s size. However, as CCUS markets take off and there is increasingly pressure for O&G companies to invest capital into the transition, Exxon is betting that the clean molecules market will scale up over time and can be an attractive business for them to build scale in. To figure out how much revenue the business can generate, it ultimately depends how much revenue per ton they can get and which services they provide. In their 2022 CCUS Business Outlook Deck, Denbury laid out 90% of volumes providing transportation and storage getting $15-$25/ton (+$10/ton when used for EOR) and 10% transportation only getting $5-$15/ton.  Current progress on Denbury’s CO2 agreements included 22 Mmtpa signed to date with a goal of >30 Mmtpa by YE2023. I anticipate this to accelerate under Exxon’s ownership as well as with their various investments and partnerships across the energy sector.

Current progress on Denbury’s CO2 agreements included 22 Mmtpa signed to date with a goal of >30 Mmtpa by YE2023. I anticipate this to accelerate under Exxon’s ownership as well as with their various investments and partnerships across the energy sector.  Denbury originally forecasted $2 billion of investments required from 2023-2030 with the ability to self-fund by 2026/2027. They estimated transport & storage volumes of 50-70 Mmtpa by 2030 resulting in an annual EBITDA of $600M-$900M+ by 2030. One obvious point that stands out is that Exxon is bigger scale, better capitalized, and has better commercial relationships to scale and ramp assets like these. Exxon appears to be betting they are better positioned to be a vertically integrated leader in the CCUS space relative to others and I'd be inclined to agree. Scale is a factor that's dominating a lot of secular tailwinds recently - Biopharma, AI, Energy Transition. It will be interesting to see if that remains the trend.

Denbury originally forecasted $2 billion of investments required from 2023-2030 with the ability to self-fund by 2026/2027. They estimated transport & storage volumes of 50-70 Mmtpa by 2030 resulting in an annual EBITDA of $600M-$900M+ by 2030. One obvious point that stands out is that Exxon is bigger scale, better capitalized, and has better commercial relationships to scale and ramp assets like these. Exxon appears to be betting they are better positioned to be a vertically integrated leader in the CCUS space relative to others and I'd be inclined to agree. Scale is a factor that's dominating a lot of secular tailwinds recently - Biopharma, AI, Energy Transition. It will be interesting to see if that remains the trend.