Data Center Headwinds: Power and... Politics?

Over 12-18 months, power constraints for AI infrastructure dominated discussion. Now, a second constraint is emerging: political resistance. This resistance can materially delay projects, inflate capex, and needs explicit reflection in bull/base/bear scenarios for value chain companies.

The Political Snowball

Last night, the vocal Senator Bernie Sanders took to twitter to declare, "I will be pushing for a moratorium on the construction of data centers that are powering the unregulated sprint to develop & deploy AI..." The Hill went on to report three Senate Democrats (Warren, Van Hollen, Blumenthal) are investigating ties between data center energy usage and rising consumer electricity bills. Two weeks ago, the NYT ran 'The New Price of Eggs.' The Political Shocks of Data Centers and Electric Bills featuring critical quotes from politicians across blue/red/purple states.

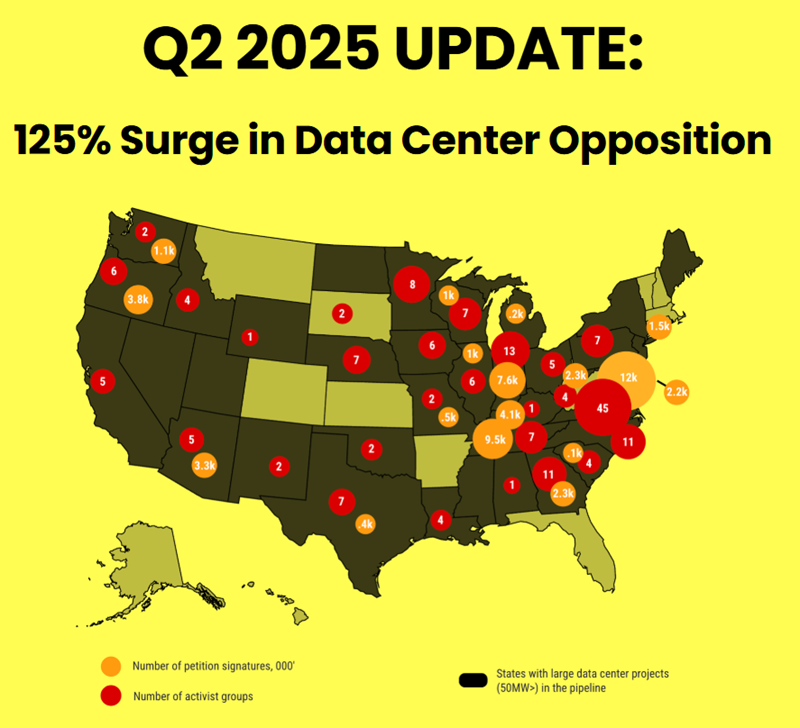

Data Center Watch's 2Q25 report: "Opposition to data centers is accelerating. In Q2 2025 alone, an estimated $98 billion in projects were blocked or delayed, more than the total for all previous quarters since 2023"

Despite White House commitment (Trump, Sacks, Wright, Krishnan), political headwinds are building toward 2026 midterms and 2028 Presidential election. The narrative writes itself: "the machines taking your jobs are also driving up your cost of living."

Investment Implications

Near-term execution matters more than long-term roadmaps. Key questions for companies:

- How many GW can you energize in 6-12 months?

- Are you working with federal/state/local regulators to prioritize projects?

- What concessions (community investments, green premiums) are you offering?

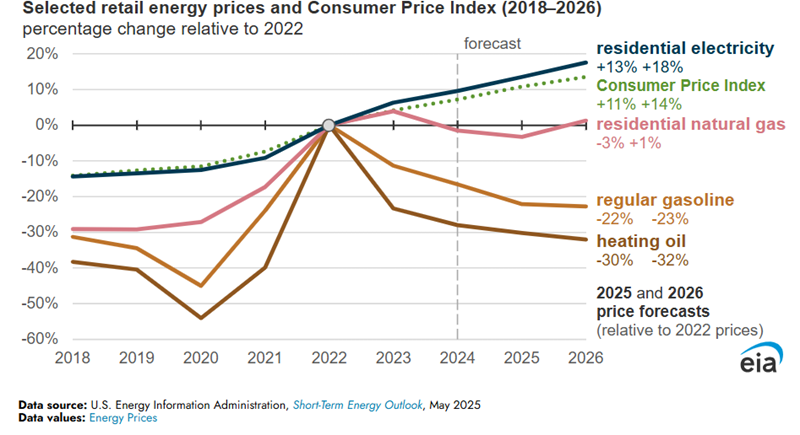

What is driving resistance? Electricity prices.

Retail electricity prices have risen faster than inflation since 2022. Media coverage manipulates y-axis scales to dramatize moves, but voter pockets feel the impact regardless. After ~20 years of flat load growth, rapid growth requires substantial new investment.

Important context: Longer-term trends (20-40+ years) show electricity prices generally kept pace with inflation, both nationally and locally. EPRI Energy Wallet data confirms this at both levels.

Nuance: Demand Growth ≠ Higher Prices

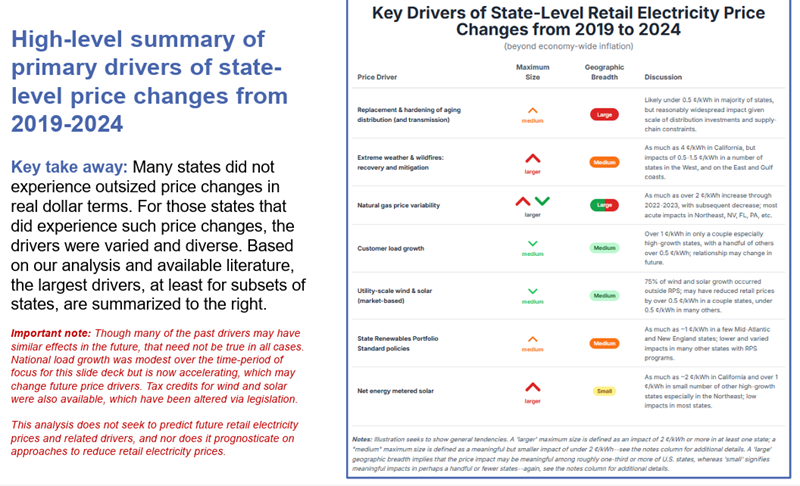

The US electricity system is a complex system with many component parts: generation stack w/ different sources, transmission, distribution, etc. and trying to isolate rises to a single variable is a fool's errand. For those that care to get into the weeds, Lawrence Berkeley National Lab (LBNL) put out an authoritative report on the drivers of electricity price changes from 2019-2024. Spoiler: Given the complex adaptive system at play, there are many factors that drive electricity price changes. Those looking for an easy "it's the data centers", "it's the solar" will be disappointed by the nuance.

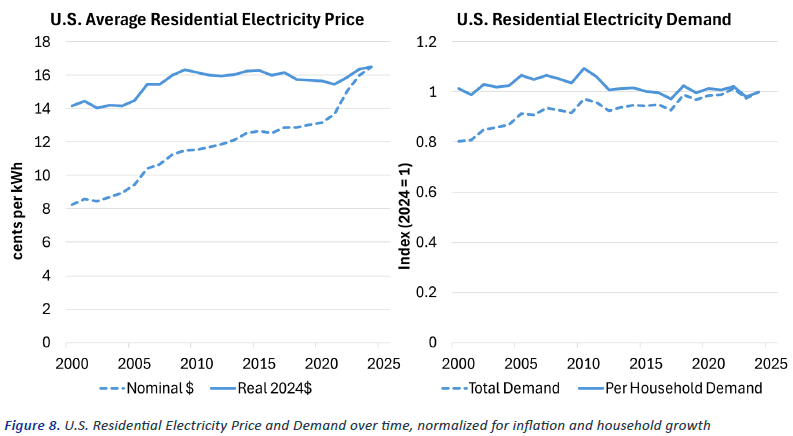

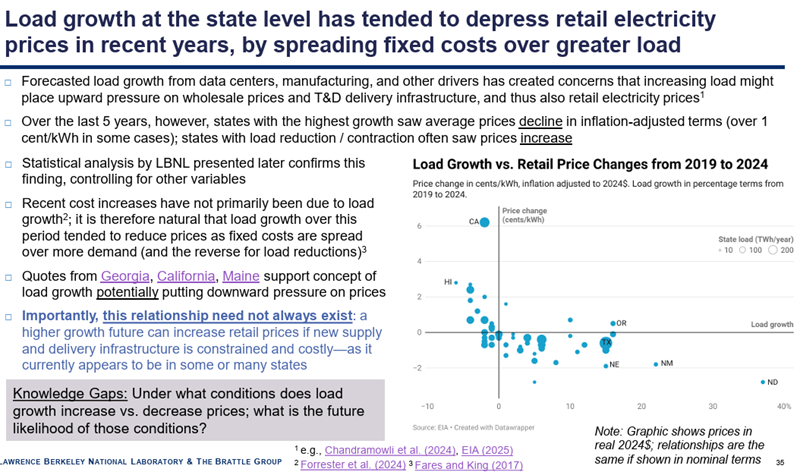

It is important to note that rising demand does not automatically = higher electricity prices. Interestingly, a 'narrative violation' is from the below from that LBNL report, which showed that over a 5Y period between 2019-2024, the states with the highest load growth saw avg. electricity prices decline in inflation-adjusted terms. Given the systems' comment above, it makes sense that more load-paying customers allow you to spread fixed costs over a higher number of paying users. This is why the buildout of the US power system is so important to get right.

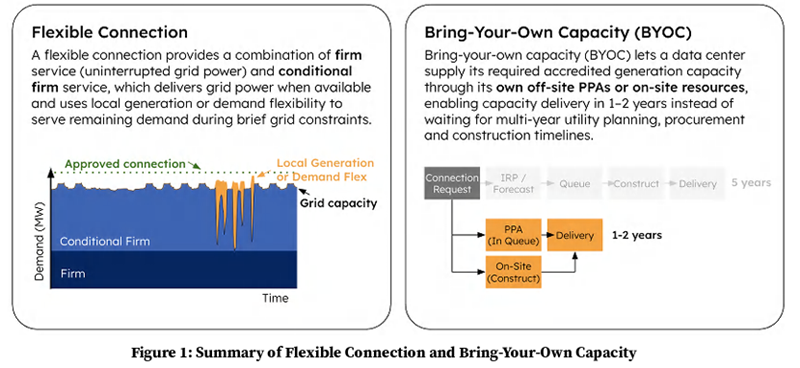

Back to data centers - while they remain a huge source of load growth in the coming years, I think they can actually be a grid asset vs. a grid liability. Data center loads are unique in the realm of power as they are flexible temporally (across time) or geographically (across space). We build our power systems around 'peaks' - the hottest summer day or the coldest winter night. We build in surplus power (e.g., ~1,200 GW of supply vs. 700-800GW peak needs today) that we can call if needed for 'worst case scenarios'. Having flexible loads means you can throttle workloads, or move them around, or deploy on-site power in scarcity events where the grid is running tight conditions. Technology companies and data center companies need to lean into this messaging to educate regulators on why they can be a part of the solution vs. the problem. If anyone wants further reading on this topic and how data centers could also solve for faster interconnect, check out the recent Camus Energy/Princeton Zero Lab report - Flexible Data Centers: A Faster, More Affordable Path to Power.

If we make regulated utilities build a bunch of new, underutilized supply, we'll end up with higher prices and stranded assets and politicians will rally against these industries. If we build a smart system that drives higher utilization, incorporates flexibility, and doesn't compromise reliability (all the above energy, flexible interconnect, and brings your own power), we can end up with lower prices and a strengthened system; and one where this sector has robust political support. It will be up to companies to educate regulators on this and ensure they don't get caught in a 'throw the baby out with the bath water situation' as data center opposition grows.