Data Centers: Focus on Energized GW in a Noisy World of Politics, Delays, and Cancellations

This serves as a follow-up to my Data Center Headwinds: Power and... Politics? post from December, given recent news reports about data delays/cancellations, growing political blowback in the US (elsewhere globally, too), and a latest view on a reasonable run-rate assumption for 2026 GW additions. Skip ahead to the sections you care about.

Politics

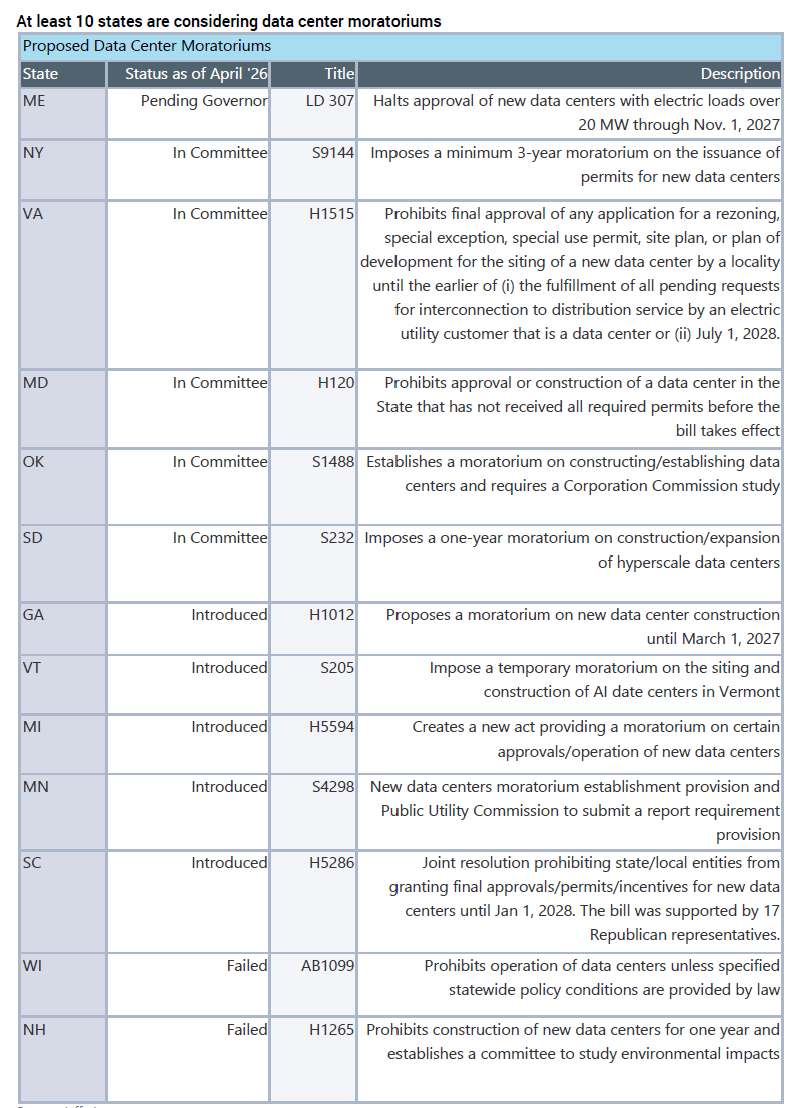

On LAST Tuesday, Maine became the first state to pass a ban on large data center construction (through legislature, awaiting governor). The bill freezes new builds over 20 MW (compared to proposed builds in the 100s to 1,000s) until November 2027 while a council studies grid and ratepayer impact. At least 15 other states are advancing similar measures. This also comes amidst recent headlines of the home of an Indianapolis city councilor shot at over his support of datacenters and a physical attack on Sam Altman's home. Data Center Watch claims projects with publicly disclosed values totaling at least $156 billion were blocked or delayed amid coordinated local opposition, moratoria, and litigation.

Much of this continues to stem from the rising electricity prices in recent years and the blame being put on datacenters. I outlined in the prior post how this is misguided — electricity prices have largely tracked inflation over decades. Every major independent study into electricity prices has confirmed it's due to a confluence of factors (FERC, LBNL) and data centers are not a meaningful contributor in historical periods; although, there is much consternation that they will contribute to future electricity price inflation.

Delays & Equipment

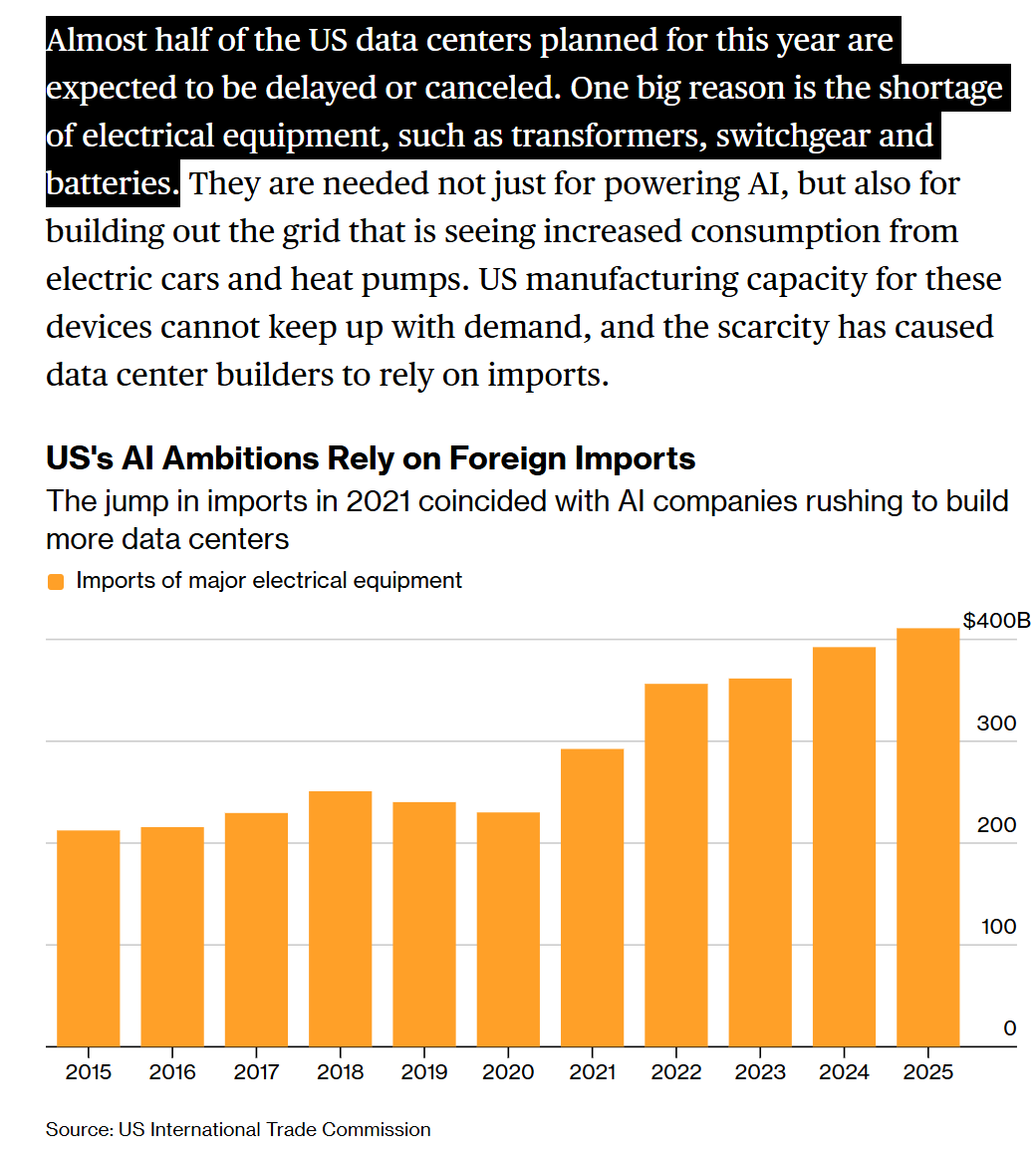

There was also a recent Bloomberg report that claimed, "Nearly half of US data centers planned for this year are expected to be delayed or canceled" and claimed it was due to severe electrical equipment shortages. That headline startled a few folks, but it's important to put it into context and why that number doesn't seem as scary as it sounds.

Interconnection queues are speculative by nature. Tying into the grid for power has always been a speculative endeavor. Historically only 13-20% of proposed projects actually get built per LBNL. Datacenters are downstream of that, and developers have been submitting applications across multiple regions and ISOs to maintain optionality, redundancy, and see who moves fastest. So, ~50% being delayed or cancelled has a natural relationship to the speculative nature of project development. It's not all equipment shortages or pricing.

That said, the delays and cost inflation are real, and they matter. We are still massively building out infrastructure. But 1-2+ year delays and ~2x+ cost increases on key equipment (power transformer unit costs up 77% since 2019 per Wood Mackenzie, distribution transformers up 78-95%) have a meaningful impact on project trajectory. Average time from interconnection request to commercial operation has more than doubled. Around 2 years for projects built in 2008. ~5 years today.

Transformer import dependencies were an issue before datacenters showed up. Much of the grid runs on aged equipment at both the transmission and distribution level. The average age of large power transformers in the US is ~40 years. 70% are 25+ years old. 55% of the ~60-80 million distribution transformers in service are older than 33 years (DOE/NREL, 2024). These businesses require skilled labor, high factory utilization to amortize costs, and expansions don't flip overnight. Equipment doesn't sell at a high margin. It's a historically low-margin, capital-intensive industry, so you live and die by cycles. The history is serious difficulties in downturns, which is why many of these businesses are focused on i) selling out capacity and ii) driving price for the first time in a long time. A lot of new capacity is being invested into, but it takes years.

We exported many of these industries decades ago. China, Korea, Mexico. In 2019, only 18% of large power transformers used domestically were produced in the US. 82% were imported (DOE/Commerce). Today imports supply an estimated 80% of US power transformer demand (Wood Mackenzie). We have a single domestic producer of grain-oriented electrical steel (Cleveland Cliffs) — none of this is new info. We stopped building and supporting domestic efforts long ago. DOE under Biden wrote multiple reports on transformer supply chain vulnerabilities far before it was relevant to talk about them for data centers.

So what? Where do we stand? What's a reasonable framework for true Energized GWs added?

There's no shortage of estimates out there on GW added, so I attempted to reconcile all the various figures floating out there to put a framework around what 'reasonable' baseline looks like, which seems to be in the mid-teens GW/year.

The installed base: FERC confirmed in their March 2026 State of the Markets report that US data center capacity exceeded 50 GW at year-end 2025. This ties to industry estimates put total US capacity in the 35-40 GW range at year-end 2024 (Bain was at ~35GW; Morgan Stanley's model pegged it at 37 GW, FERC closer to 40GW). That implies roughly +10-15 GW of net additions in 2025, a massive step-up from prior years. As a disclaimer, total facility power, critical IT load, and hyperscale cited GW all produce different baselines. I haven't seen two sources use the same definition consistently.

Frontier labs: On recent podcasts, Brad Gerstner (investor in both OpenAI and Anthropic) said OAI and Anthropic have 1.5-2 GW each today, going to ~5 GW by year-end. Dylan Patel at SemiAnalysis said both were at roughly 2-2.5 GW today and that both reach 5-6 GW by year-end 2026 with OpenAI slightly higher. Dylan claimed each were targeting ~10 GW by end of 2027. Sarah Friar (OpenAI CFO) confirmed 1.9 GW for OpenAI at year-end 2025. Fair to assume Anthropic's operational capacity is likely in the 1.5-2 GW range.

On year-end targets, there's a wide gap between what's been contracted under framework agreements (e.g., Stargate, NVIDIA partnerships, CoreWeave deals, Google TPU) and what will physically be energized by December. Per Dylan, Anthropic was conservative on locking up compute early while OpenAI signed aggressively so Anthropic has to now pay rental rates or go to lower-quality providers to catch up (but Gerstner's comments made it sound like the take rate wasn't that high — he said single digits). Of note, neither leading lab owns or builds data centers today so their ~6 GW of combined incremental capacity in 2026 is physically built and operated by AWS, Google, Microsoft, CoreWeave, Oracle, which makes it difficult to attribute every incremental GW to ultimate end user of that capacity.

Hyperscaler disclosures on physical delivery: As discussed, these are a mix of US and global figures, and facility power vs. IT load definitions vary across companies, so hard to compare apples-to-apples but worth detailing.

- Amazon (AWS): Disclosed AWS added 3.9 GW of new power capacity in 2025 (1.2 GW in Q4 alone). Operating from a base of roughly ~8 GW at year-end 2025, with a target to double total capacity by year-end 2027 implying ~16 GW total.

- Microsoft (Azure/Co-Pilot): Team disclosed over 2 GW added in FY2025, with roughly 1 GW brought on in the December quarter alone. Also targeting roughly double capacity by 2027. SemiAnalysis reported that Microsoft paused over 3.5 GW of capacity that would have been built by 2028, though Reuters/TD Cowen put the figure lower at ~2 GW of abandoned projects in the US and Europe over a six-month period (a mix of deferrals and cancellations, with explicit terminated leases of only ~200 MW), and Bernstein says actual cancelled contracts total only "a couple hundred megawatts". The directional point is clear that Microsoft was recalibrating its self-build vs. lease mix but now seems to be building again.

- Google (Alphabet/GCP/Gemini): Guided 2026 capex at $175-185B, nearly double 2025. No explicit "we added X GW" disclosure comparable to AWS/MSFT. Dylan describes them as "still capacity constrained" and acting fast — buying an energy developer (e.g., Intersect), putting down turbine deposits for 2028-29, negotiating long-term power agreements across multiple generation sources, and signing demand response deals with utilities for faster interconnect times. Without a disclosed GW figure, I'd estimate 3-5 GW of 2026 additions based on capex trajectory similar to MSFT or AWS.

- Meta (MSL): Guided $115-135B in 2026 capex, materially higher than 2025. Self-build pipeline includes the 1 GW Prometheus campus in Ohio coming online in 2026, with longer-dated builds at the 1 GW El Paso campus (investment scaled from $1.5B to $10B, targeting 2028), the 1 GW Lebanon, Indiana campus, and the Louisiana JV with Blue Owl (~$27B, scalable to 5 GW). On top of the self-build, Meta has committed $35.2B to CoreWeave across two deals for third-party capacity, though only the original $14.2B Sept 2025 deal is relevant to near-term 2026/2027 capacity; the additional $21B April 2026 expansion runs 2027–2032 and includes early Vera Rubin deployments.

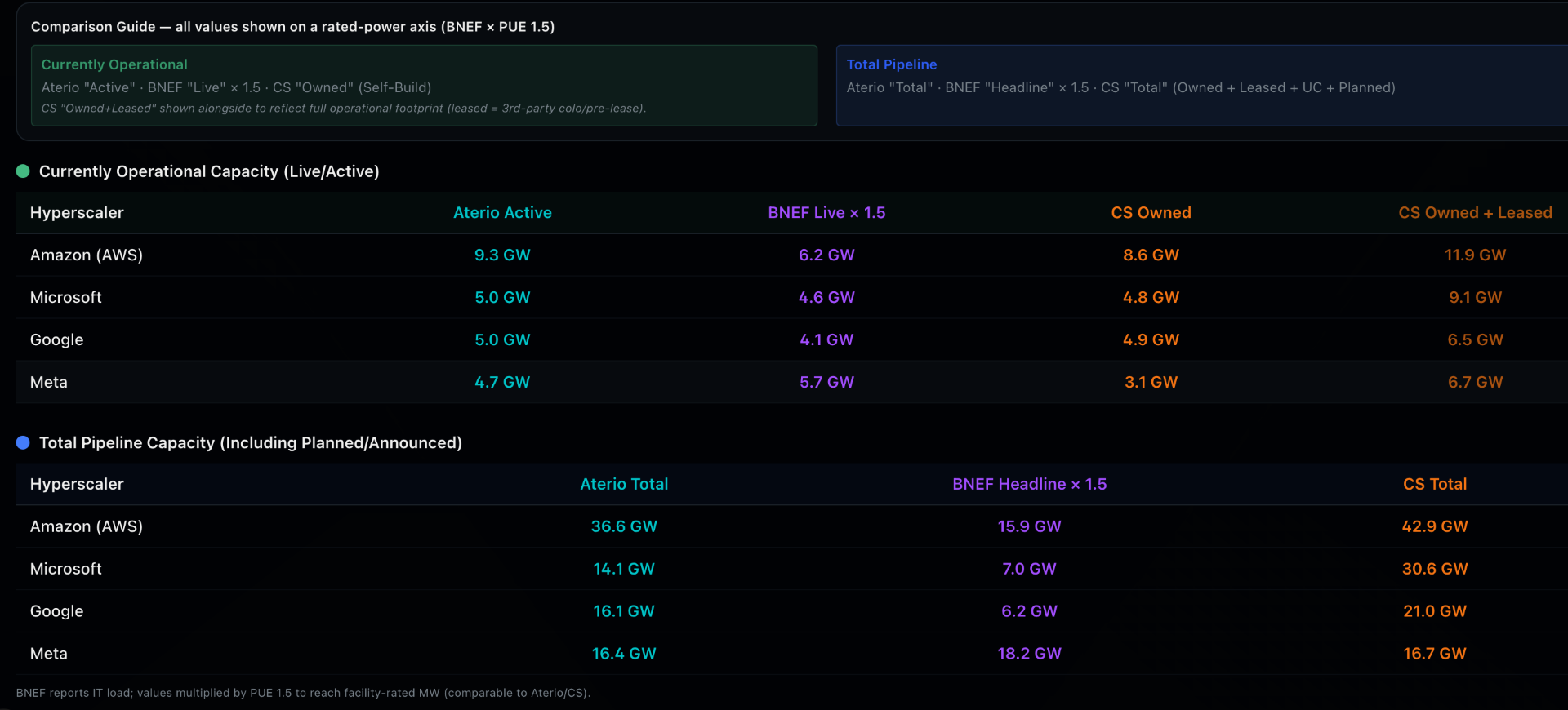

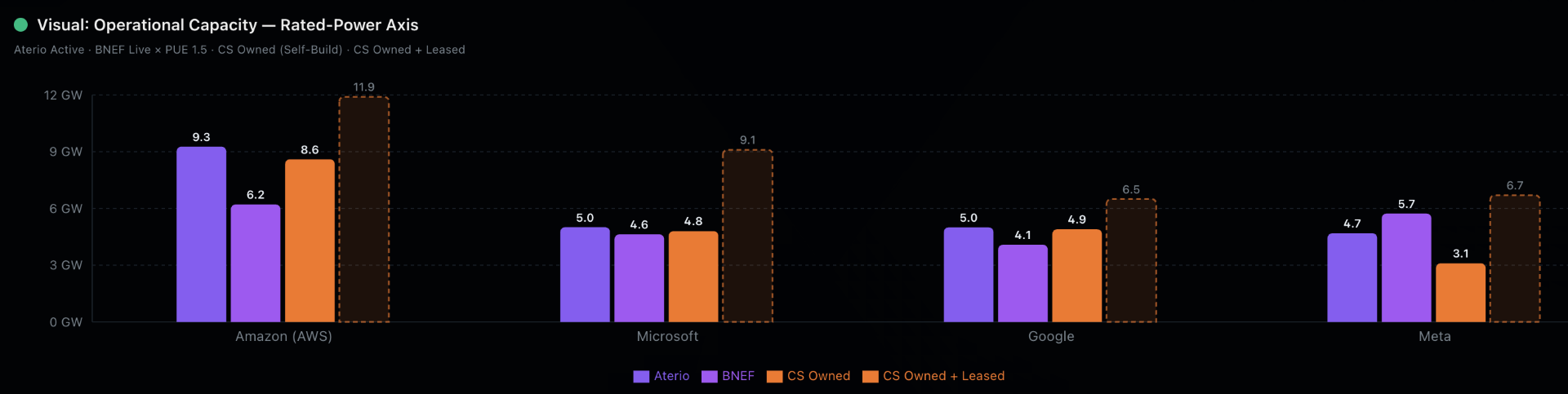

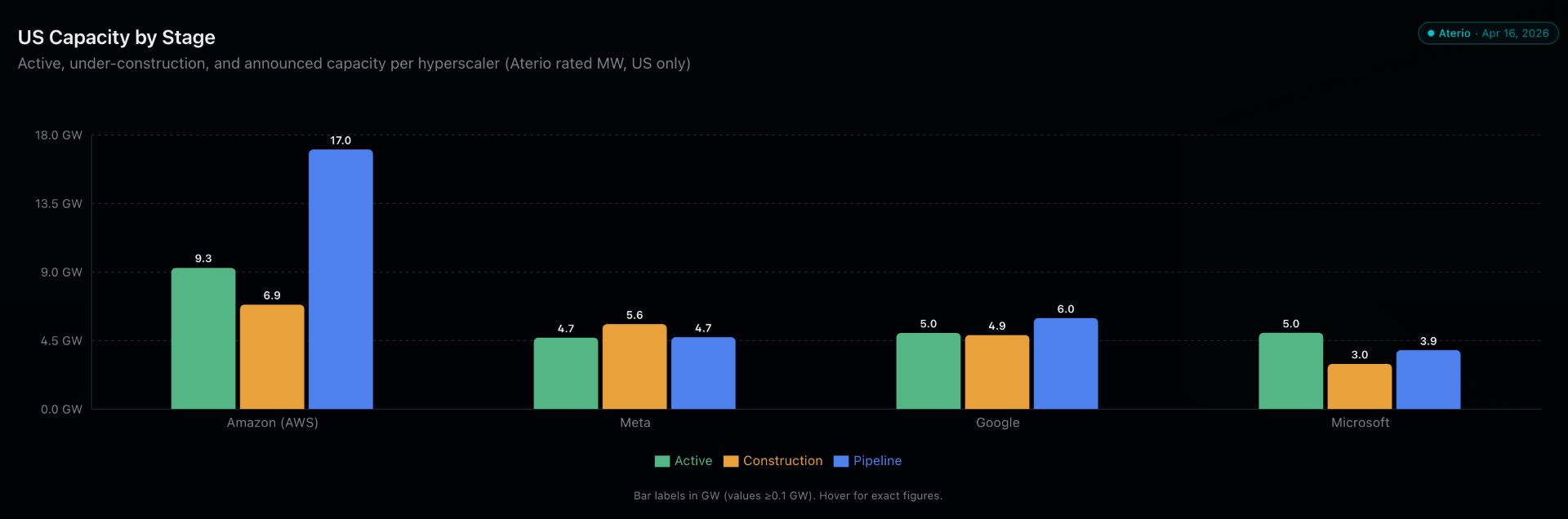

For the data sources I have access to (e.g., Aterio, DCByte, DatacenterHawk — static as of Dec-25), here is a comparison view of active vs. under construction vs. pipeline data for the hyperscalers. Pipeline views are not particularly helpful as they are very inflated by double/triple-counting or speculative projects (e.g., aggregate national forecasts paint widely divergent pictures, with Wood Mackenzie reporting a 241 GW disclosed pipeline, Eaton estimating 165-200 GW through 2030, ERCOT reported a 368 GW figure this week vs. multiple analysts and third-party forecasts projecting actual realized demand of ~100 GW by 2035 or <25% of a gross pipeline).

Independent builders and neoclouds:

- Musk's xAI: Colossus 2 in Memphis is targeting 1-2 GW of capacity to support 550,000 next-gen Nvidia chips, scaling to 1 million GPUs. Deployed 35 natural gas turbines generating 420 MW behind the meter to work around grid constraints.

- CoreWeave: Team added 490 MW across 11 data centers in 2025 (260 MW in Q4). Total active capacity hit 850 MW at year-end against 3.1 GW contracted. Planning $30-35B of 2026 capex. Also acting as a lead builder on the 1.2 GW Stargate Abilene campus for OpenAI.

- Nebius: Tracking toward 800 MW - 1 GW of available capacity in 2026. Meta signed a five-year agreement for $12B of dedicated AI computing capacity from Nebius starting in early 2027, with an option for up to $15B of additional capacity over five years (up to $27B total).

Sense-checking the total — A few different ways to triangulate:

- Morgan Stanley: Forecasts ~24 GW of global additions in 2026 × 50-60% US = ~13-14 GW.

- BloombergNEF: Outlook had +~8-10 GW of IT Load × 1.3-1.5 PUE = ~12-14 GW.

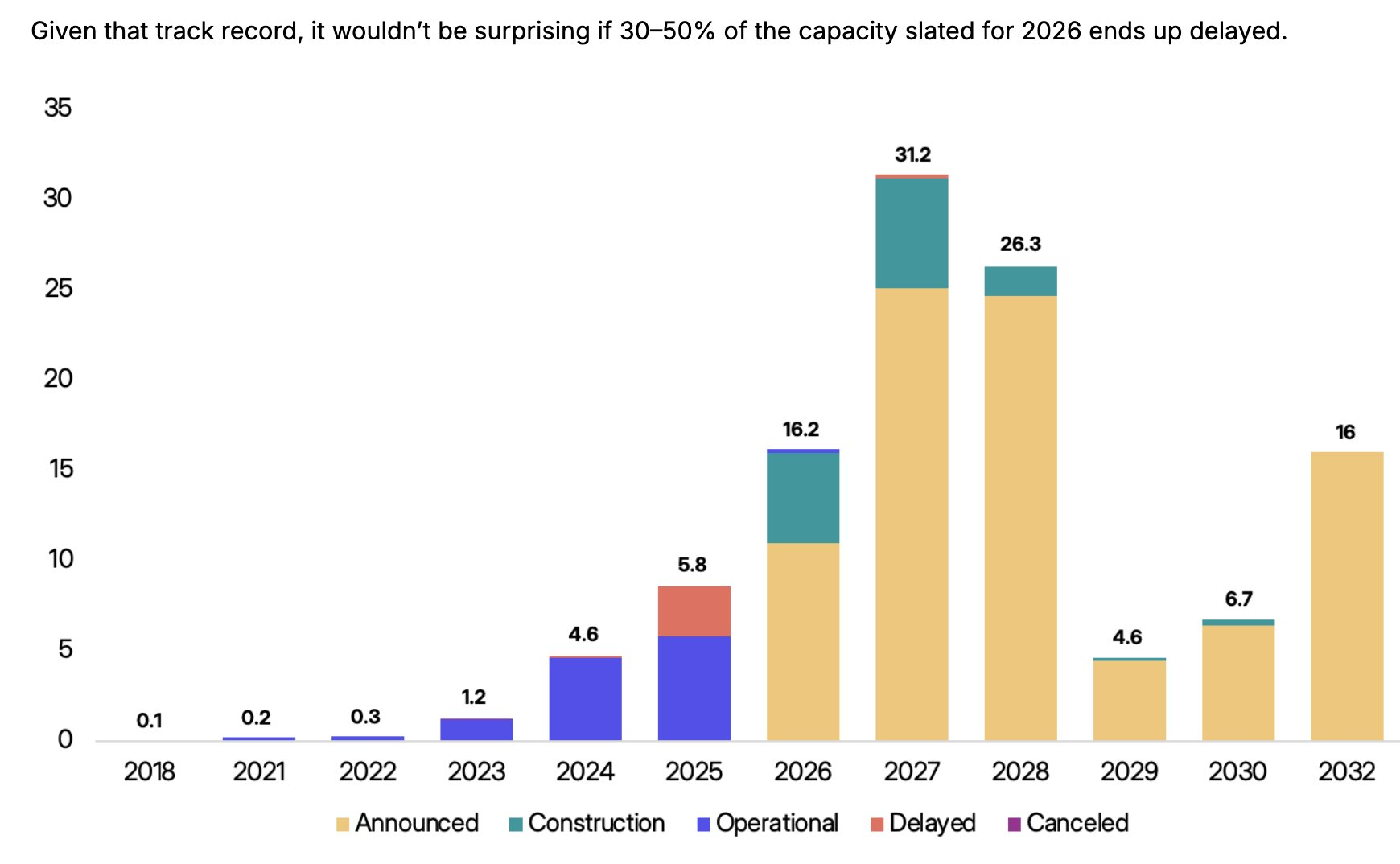

- Sightline: Shows at least 16 GW of US data center capacity slated to come online in 2026 across 140 projects but warns 30-50% may face delays due to power constraints and equipment shortages.

- Crude capex BOTE math: $600-700B in 2026 hyperscaler capex at roughly $40-50B per GW cost of fully built capacity also implies mid-teens GW. That's an imprecise conversion as capex covers equipment, data center shells, chips, and land that enter service across different years but it provides another directional anchor.

- Colliers: Reported that North American data center absorption hit 15.6 GW in 2025, double the 2024 level.

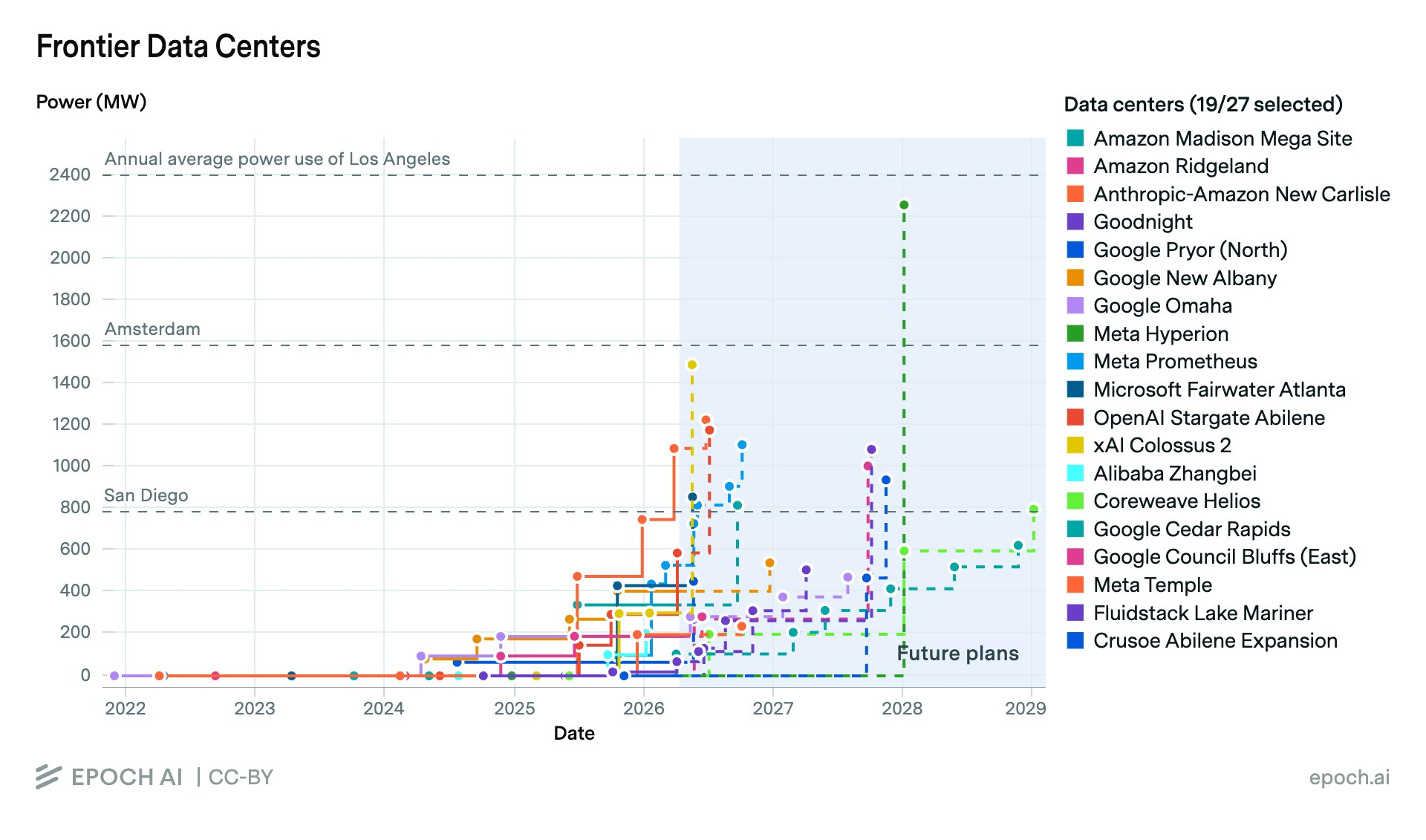

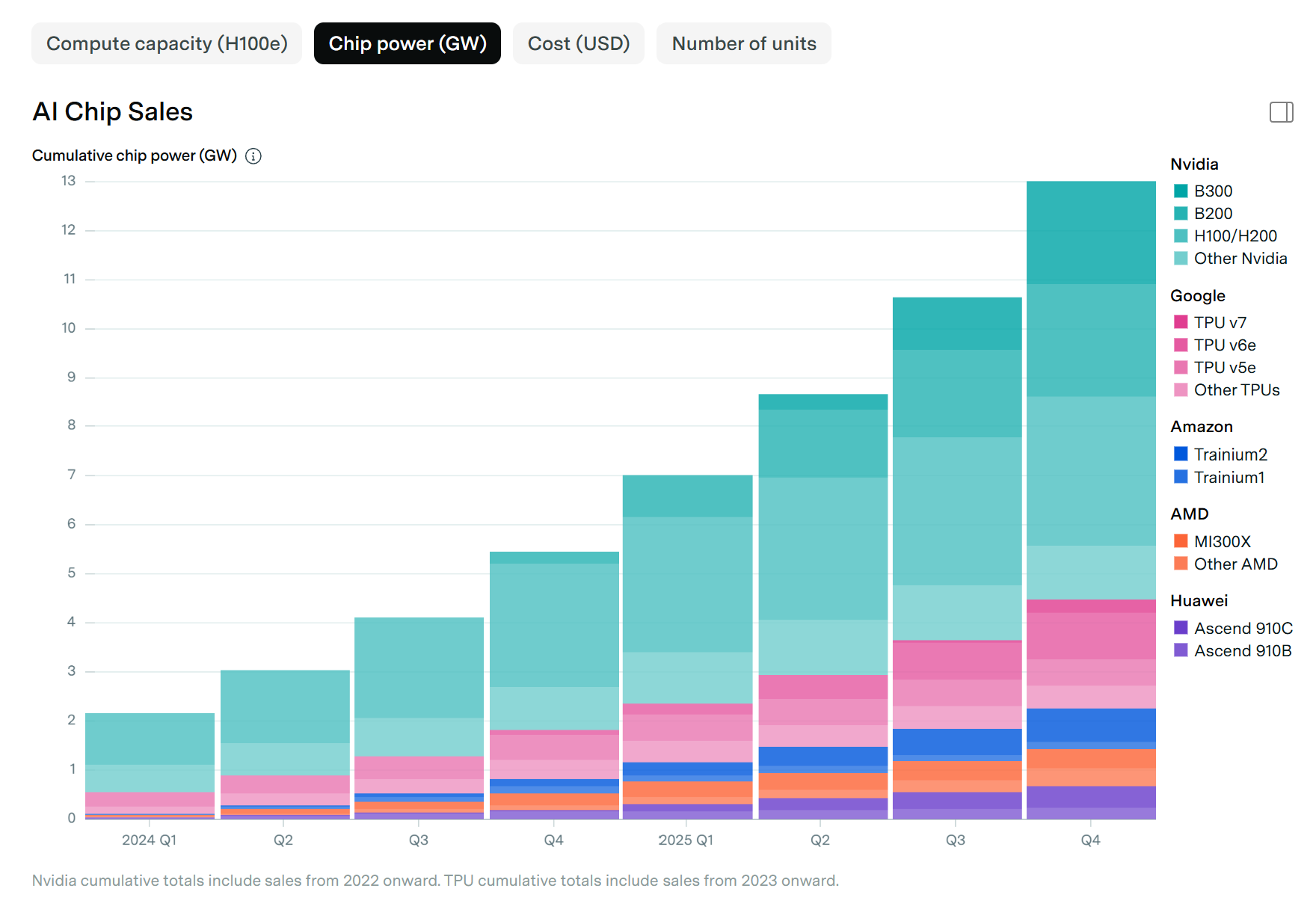

- Epoch AI: Frontier data center tracker confirms the step-function: most of the largest campuses (e.g., Meta Hyperion at 2.2 GW, Microsoft Fairwater above 1 GW) don't fully arrive until 2027-2028. They also track chip data and show ~13 GW cumulative power capacity across all providers since 2021.

It seems a reasonable base case for actual 2026 US net energized capacity additions: ~15-20 GW. Importantly, constraints are piling up — skilled labor (mechanical, electrical, plumbing), grid interconnection, electrical equipment, memory, etc. — and now you have the political angle developing aggressively, so it's important to track what could derail that figure and what we are underwriting in future estimates.